Working capital is the amount of money a company needs to finance its daily operations. It comes straight from the balance sheet and so represents that moment in time. Managing working capital well can improve your company’s profitability and its cash position.

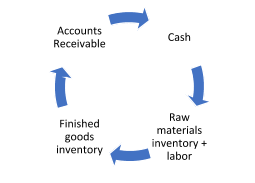

The company uses cash to purchase raw materials and hire labor, produces the service and (if it is a product is becomes inventory) and then creates an account receivable to bill for the service. The cycle is complete once the account receivable is collected.

This is the company’s operating or working cash cycle.

This is your cash flow production cycle. If this cycle is interrupted or limited, the company can become insolvent. Note that a company could be profitable and still be insolvent. Here are two examples:

- Company A is selling services for a profitable price but providing those services far ahead of the time it collects its accounts receivable. Eventually, it could become insolvent.

- Company B is managing its inventory and receivables carefully, but it is experiencing rapid sales growth which forces larger investments in materials and labor. It may have too little cash to meet obligations and could be “growing broke”.

Measuring Working Capital

Accountants usually measure working capital using this formula:

Working capital = current assets – current liabilities.

How the Working Capital Requirement affects the bottom line in the Sale of your Business

Buyers of small privately-held companies are usually making their offer for a going-concern on a “cash-free, debt-free” basis. Sellers are expected to pay off all their debts prior to closing. Sellers will keep cash and accounts receivable in the business at closing less a working capital amount. That working capital is likely defined as “a normal level of working capital” and in the Purchase Agreement is often called the Target Working Capital amount. If the working capital at closing is less than the target, the seller will have to pay the buyer (or leave those assets in the business). If the working capital at closing is more than the target, the buyer would pay the difference.

This working capital requirement is intended to prevent the seller from stripping all the capital from the business prior to closing. Since the business is a going-concern, it should generate cash to fund normal operations. Buyers do not expect to finance working capital for normal operations in addition to the purchase price.

The Target Working Capital number is typically based on the average working capital for the company for the past twelve months that generated the EBITDA that the purchase price was based on. Using twelve months is intended to smooth out seasonal changes. While there are a number of strategies that can be used to define the target number (Seller preferring a lower target and Buyer preferring a higher number) this can be a challenging negotiation area because it involves accounting, law and finance as well as the buyers and sellers. Ideally, the parties will document their understanding early in the process to avoid misunderstandings later.

If you would like to discuss your situation on a confidential basis, call Alison at 224-688-8838 or email me at [email protected]. We’re here to help you harvest your potential.